First-time homebuyer grants offer financial support to low- and moderate-income individuals looking to buy a home. These grants are cash awards that do not require repayment, making them valuable resources during the initial financing process.

“We frequently see prospective homebuyers who can afford to make a monthly mortgage payment but are unable to accumulate enough funds for a down payment and closing costs,” said AJ Barkley, a lending executive at Bank of America.

Not all first-time homebuyers are eligible for grants, and not all grants go to people who are commonly considered first-time homebuyers. The Department of Housing and Urban Development (HUD), along with lenders and assistance programs, define a first-time buyer as someone who hasn’t owned a home in the past three years.

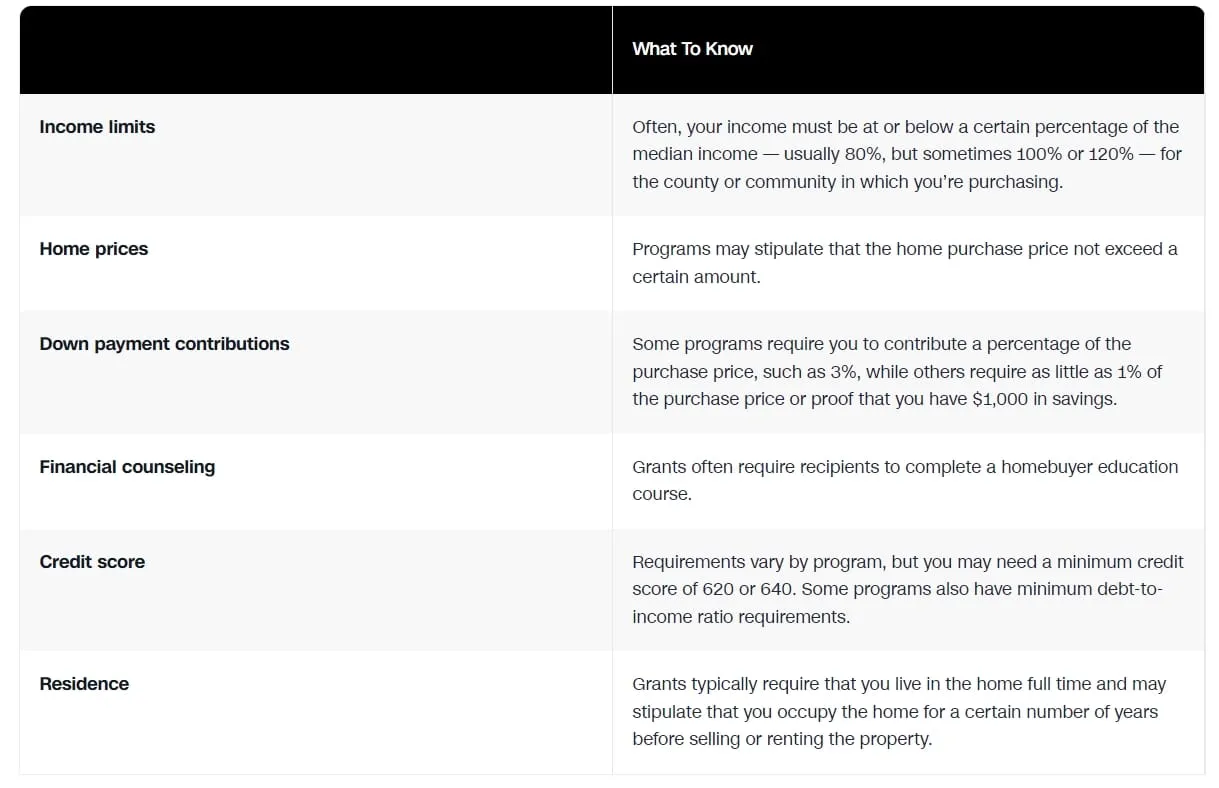

Eligibility requirements for homebuyer grants

Eligibility for borrowers usually includes income limits, with many programs targeting households earning 80% or less of the area's median income. To qualify for a grant, you might also need to purchase a property within a specific location and below a set maximum sales price. Additionally, these programs often have minimum credit score requirements.

Different types of first-time homebuyer grants

Homebuyer grants are essentially strings-attached cash allotments to put toward the purchase of a home. And they come in several forms, including:

- Down payment assistance: Programs vary in the amount of assistance offered, but grants can range from $5,000 to $15,000 and up.

- Closing cost assistance: Grants may offer one lump sum for both down payment and closing cost assistance. Alternatively, they may cover just closing costs (such as home appraisal, title insurance and recording fees), which typically run 2% to 5% of the home’s purchase price.

- Interest rate discount: Some programs, such as the Federal Housing Finance Agency’s first-time homebuyer mortgage rate discount, waive loan-level pricing adjustments (that raise the interest rate over the life of your loan and are based on your credit profile and other lending risk assessments).

- Forgivable loans: Forgivable loans come with an interest rate of 0% and don’t have to be paid back as long as you meet program criteria and conditions.

- Tax credits: Some first-time homebuyer programs offer mortgage tax credit certificates, known as MCCs, which provide qualifying homebuyers a nonrefundable federal tax credit equal to a percentage of the interest paid on their mortgage loan.

How to apply for a first-time homebuyer grant

Though eligibility criteria and application processes vary by grant program, start with these steps:

- Qualify for a mortgage. Generally, grant recipients must qualify for a mortgage to be eligible for grants. Once you select your preferred home loan type (such as conventional versus FHA), compare offers from multiple lenders to get the best mortgage rate and terms for your situation.

- Start your grant search. Research grants available in your state, city or county. This will give you an idea of eligibility rules for local grant programs and how the additional funding would support your overall budget.

- Review relief programs with your lender. “Meeting with a lending specialist is the best first step to confirm your status and see if you qualify for any assistance programs,” Barkley said. “In fact, you’ll likely find many down payment assistance programs do not require you to be a first-time homebuyer or, depending on the program, there may be other benefits that you are eligible for.”

- Keep seeking out aid online. Search for grant programs, such as HUD’s database of down payment assistance programs run by nonprofit organizations.

- Prep your application materials. Many grant programs require extensive applications and documentation, so aim to promptly fulfill the requirements to keep the process moving along.

Tips for first-time homebuyers

Consider the following guidance as you plan your home purchase:

- Think local. Your state, city and county may offer grants — and your local bank or credit union might, too. Some programs are geared toward public servants and military personnel, so check for grants that may be specific to your employment.

- Be patient. Some first-time homebuyer grant programs involve stacks of paperwork that can slow down the closing process, so be prepared and exercise patience.

- Consider a low-down-payment mortgage. Whether you qualify for a grant or not, a low-down-payment mortgage can help you achieve a home purchase. Fannie Mae’s HomeReady program and Freddie Mac’s Home Possible each offer 3% down payment mortgages, which are even lower than those backed by the FHA.

- Investigate other types of aid. Other grant alternatives include down payment assistance loans, deferred payment loans and loan forgiveness.